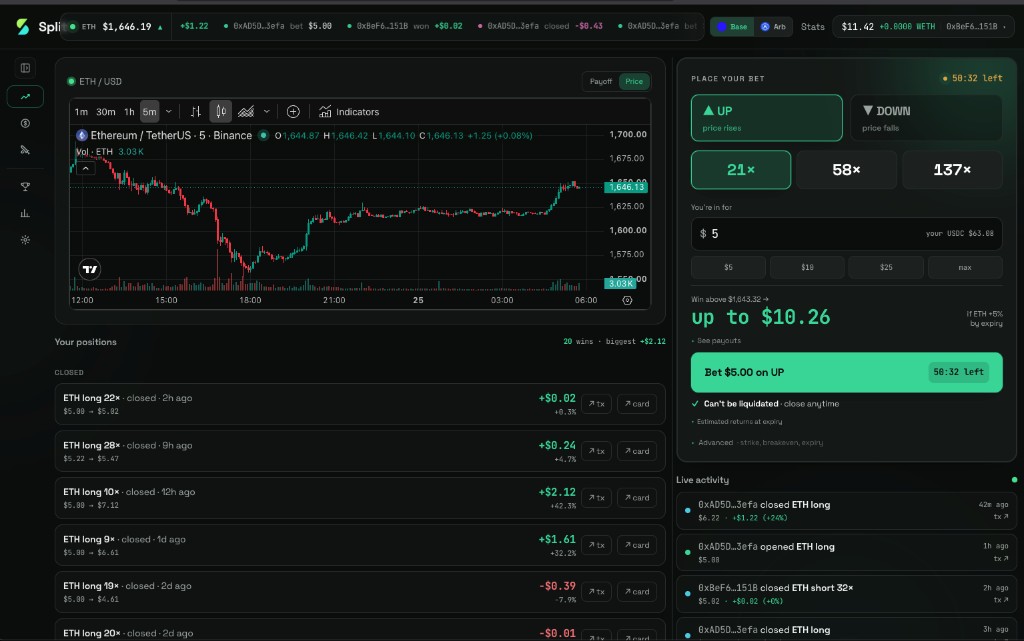

What is Split (vs perps)

If you trade perps, Split is the same intent, leveraged exposure to ETH, with a different risk shape. You go UP or DOWN with a leverage tile, the way you would long or short a perp. You keep the upside leverage. You trade away liquidation and funding for a fixed up-front cost and an expiry. You can still close any time, your position just can't be liquidated.

Side by side

| Perp | Split | |

|---|---|---|

| Max loss | Your whole margin (liquidation) | The premium you paid, and nothing more |

| Liquidation | Yes, a wick can wipe you | None. There is no liquidation engine |

| Ongoing cost | Funding rate (variable, can flip) | Theta, paid once, up front, inside the premium |

| Time limit | None (perpetual) | An expiry (the option settles) |

| Upside | Linear with leverage | Leveraged, convex above breakeven |

| What you hold | A margined position | N, an on-chain option token you own |

Why no liquidation is the headline

On a perp the danger is not being wrong, it is being temporarily wrong. A sharp wick hits your liquidation price and you are closed at the worst moment, even if price snaps right back.

On Split there is no liquidation price. You buy the position, your loss is capped at the premium, and you survive the wick. The position only resolves at expiry.

ETH price over your hold

│ ╱╲ ← a wick spikes against you

│ ╱╲ ╱ ╲ ╱╲

│ ╱ ╲╱ ╲ ╱ ╲___

│ ╱ V ← perp gets liquidated here

│

└────────────────────────▶ time

Split: nothing happens here. Only the price at expiry matters.What you pay for it

- Theta. Time decay is real. If ETH goes nowhere the premium erodes, and an out-of-the-money option can expire worthless. That is the cost of the no-liquidation structure.

- An expiry. This is not a position you hold forever. It settles. You close early, let it auto-exercise (calls), or it expires.

When a perp fits better

- You want to hold a directional position indefinitely with no expiry.

- You expect a slow grind in your favor where theta would eat an option.

- You want exact linear exposure with no premium convexity.

Split fits when you want defined risk through volatility: leveraged, un-liquidatable, with a cost you know before you click. Next: open an UP position.